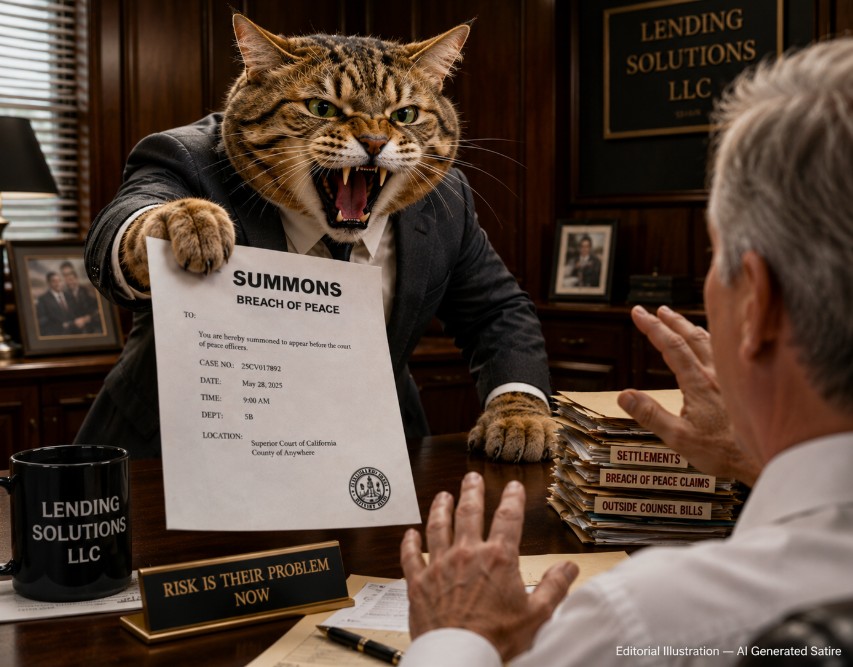

Why the Repossession Industry May Be Encouraging the Very Claims It Wants to Prevent

Feeding Stray Cats – When Settling Becomes the Problem

The repossession industry has spent decades improving professionalism.

Agents receive more training than ever before. Cameras record assignments. GPS logs document vehicle movements. Compliance standards continue to evolve. Yet despite these efforts, one category of litigation seems to remain stubbornly persistent: breach-of-peace claims filed months after a recovery has already been completed.

Many recovery professionals have noticed a pattern.

The repossession occurs.

The vehicle is sold.

Months pass.

Then the borrower receives a deficiency balance letter informing them they still owe money on the loan.

Suddenly, allegations emerge that the repossession itself was improper.

Whether the timing is coincidence or cause is impossible to know in every case. What is clear, however, is that these claims frequently arrive long after the events in question and often after memories have faded, witnesses have moved on, and evidence becomes more difficult to obtain.

The industry’s response has created a troubling dynamic.

For many lenders and insurers, settling such claims is simply a business decision.

A defense may cost tens of thousands of dollars. A settlement may cost less. The file closes. The risk disappears.

At least for the lender.

For the repossession agency, the consequences often remain.

The agency may be asked to contribute toward the settlement. Insurance premiums may increase. Vendor relationships may be jeopardized. Reputational damage can linger long after the case is closed.

In some instances, the lender who authorized the recovery escapes with minimal disruption while the recovery company bears the long-term consequences of a claim that was never fully litigated or proven.

This creates a fundamental question:

If allegations can generate settlements without rigorous examination, what incentive exists to discourage questionable claims?

The comparison may be uncomfortable, but I’ve always described the situation of settling frivolous or unsubstantiated claims as feeding stray cats.

Leave food on the porch often enough and eventually more cats arrive.

The issue is not legitimate claims. Genuine breach-of-peace incidents should be taken seriously. They expose consumers, lenders, and recovery agents to significant risks. The industry has an obligation to identify and address those situations whenever they occur.

The concern arises when settlements become routine.

Over time, a predictable settlement environment may unintentionally encourage additional claims. Plaintiff attorneys learn where insurers are willing to negotiate. Borrowers learn that allegations may produce compensation. The economic incentives begin favoring litigation rather than fact-finding.

Meanwhile, the industry rarely examines what happens after the settlement.

How many claims were supported by independent witnesses?

How many involved police reports?

How many had contemporaneous complaints?

How many were dismissed when challenged?

How many resulted in findings of actual wrongdoing?

The truth is that the repossession industry lacks reliable data on these questions.

For an industry increasingly driven by analytics, performance metrics, and compliance reporting, there is surprisingly little visibility into breach-of-peace claim outcomes. Agencies know their own experiences. Lenders know theirs. Insurers know theirs. But few see the larger picture.

Perhaps it is time to start.

The industry might benefit from greater documentation standards, stronger evidence preservation, and a more collaborative approach between lenders and recovery vendors when claims arise. Settlements may sometimes be appropriate, but they should not automatically become substitutes for investigation.

Technology can help.

Body cameras, vehicle cameras, GPS tracking, timestamped photographs, and digital communication records provide opportunities to evaluate allegations based on evidence rather than assumptions. Agencies that can reconstruct an assignment months later are often in a far stronger position than those relying solely on recollections.

Lenders also have an important role to play.

If a lender chooses to settle a claim, the decision should not automatically become a verdict against the recovery company. Agencies deserve transparency regarding the basis for the settlement and an opportunity to participate in the defense of allegations that may affect their future.

The current system often allows one party to purchase certainty while another absorbs the consequences.

That arrangement serves no one well.

The repossession industry cannot eliminate litigation. Nor should it attempt to discourage legitimate complaints. Consumer protections exist for a reason, and breach-of-peace laws remain an essential safeguard.

But there is a meaningful difference between protecting consumers and creating an environment where allegations become economically attractive regardless of merit.

If the industry truly wants to reduce breach-of-peace claims, it may need to look beyond training manuals and compliance programs. It may need to examine the incentives surrounding settlements themselves.

Because when every problem is solved with a check, the lesson being taught may not be the one the industry intends.

We teach people how to treat us.

And until that changes, many recovery professionals will continue to feel as though they are operating under an increasingly familiar reality: Recovery completed – Lawsuit pending.

Feeding Stray Cats – When Settling Becomes the Problem – Feeding Stray Cats – When Settling Becomes the Problem – Feeding Stray Cats – When Settling Becomes the Problem

Kevin Armstrong

Publisher

Feeding Stray Cats – When Settling Becomes the Problem – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Lawsuit – Lawsuit

More Stories

The Cost of Doing Everything Right

Recovery Completed – Lawsuit Pending

The Repossession Industry’s Missing Asset: Institutional Memory

Should Florida Repossessors Be Allowed to Carry Firearms?

The Future of Repossession Forwarding Depends on Recovery Agencies

When the Watchdog Leaves: What a Smaller CFPB Could Mean for Repossession