Minnesota’s HF3856 Could Make LPR Worthless Overnight

Hardly a year goes by without one state or the other proposing a way to kill License Plate Recognition data from being gathered and used by the repossession industry. This time, it’s a Minnesota bill targeting LPR use that could completely upend repossession industry practices, leaving repo agents, lenders, and recovery firms searching for answers and alternatives.

Minnesota HF3856 (introduced March 2, 2026, and referred to the House Judiciary Finance and Civil Law committee) creates new restrictions on Automated License Plate Recognition (LPR) systems in proposed Minnesota Statutes § 325M.40.

Read the Bill Here!

It bans government entities (including law enforcement except with a judicial warrant) from using LPR systems or accessing private LPR data, repeals prior statutes (Minn. Stat. §§ 13.824 and 626.8472) that allowed limited law enforcement use, and requires deletion of existing law enforcement LPR data within seven days.

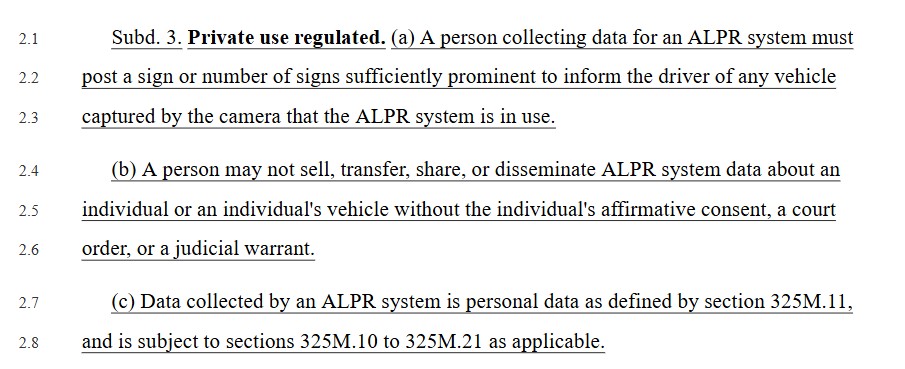

The provisions most relevant to the repossession industry (private tow/ repo companies, agents, and third-party LPR service providers they rely on) are in Subdivision 3 on “Private Use Regulated”:

- Any “person collecting data for an LPR system” must post prominent signs informing drivers that LPR is in use.

- No person may sell, transfer, share, or disseminate LPR data about an individual or their vehicle without the individual’s affirmative consent, a court order, or a judicial warrant.

- LPR data is treated as “personal data” under the Minnesota Consumer Data Privacy Act (MCDPA, Minn. Stat. §§ 325M.10–325M.21) and subject to its requirements “as applicable.”

Repossession companies and their vendors (e.g., services providing mobile LPR on tow trucks, fixed-camera networks, or “hot list” alerts for specific plates) fall squarely under these private-use rules.

Key Challenges for the Repossession Industry

- Signage Requirement Makes Covert Operations Impossible

Mobile LPR on repo trucks or agent vehicles would require visible signs on every truck or at every scanning location. Fixed-camera networks used by commercial services would need signs at every deployment site. This alerts debtors, increases vehicle hiding/evasion, raises safety risks during repossessions, and undermines the entire purpose of LPR (quick, low-profile location). Posting signs everywhere is logistically burdensome and may deter property owners from allowing cameras. - Data-Sharing and Dissemination Ban Effectively Blocks Industry Standard Practices

Repossessors cannot receive location “hits” or plate data from third-party LPR vendors without the debtor’s consent (which will never be given) or a court order/warrant for each query or alert. Internal sharing of results with the client lender/lessor, or even between repo agents and their dispatch, could violate the rule. This kills the commercial LPR model that most Minnesota repossession firms depend on. Alternatives (manual surveillance, public records, GPS if installed) are slower, far more expensive, and less effective, leading to lower recovery rates, higher storage/holding costs, increased risk of asset damage or concealment, and more “breach of peace” incidents. - Compliance Overlay Adds Significant Burdens and Costs

Even if a small repo firm qualifies for MCDPA’s small-business exemption, the bill’s explicit rules still apply. Larger operators or vendors become “controllers” and must:- Provide privacy notices to every scanned driver (impractical at scale).

- Honor consumer rights (access, deletion, correction, opt-out of processing/sale/profiling).

- Conduct data privacy assessments, implement security, limit collection/retention, etc. Debtors could demand deletion of their plate data or logs of scans, disrupting ongoing investigations. No carve-outs exist for debt collection, secured transactions, or repossession activities.

Overall operational impact: Higher costs passed to lenders (and ultimately consumers via higher rates/fees), slower turnaround, more failed or litigated repossessions, and potential business model collapse for firms relying heavily on LPR.

Potential Legal Infringements or Conflicts

HF3856 does not explicitly ban repossession or directly conflict with Minnesota’s adoption of UCC Article 9 (Minn. Stat. Ch. 336), which allows self-help repossession of collateral after default without judicial process (as long as there is no breach of the peace). However, it creates severe practical impairments:

- Requiring court orders or warrants to access location data for routine collateral recovery effectively forces many repossessions into the judicial system, undermining the “self-help” right that UCC § 9-609 was designed to preserve. Lenders and repossessors could argue this impairs contractual expectations and security interests in a way that raises constitutional concerns (e.g., impairment of contracts under U.S. Const. Art. I § 10 or state equivalents, or due-process burdens on property rights).

- Violations of the sharing ban or signage rule expose operators to enforcement under the new statute (and potentially MCDPA penalties up to $7,500 per violation via the Attorney General; no private right of action under MCDPA itself). Continuing current practices post-enactment would risk civil or administrative liability.

- Interstate LPR service providers serving Minnesota clients could face compliance dilemmas, potentially triggering Commerce Clause challenges if the law unduly burdens out-of-state commerce.

- No exemptions or savings clauses for repossession, debt collection, or secured-creditor activities appear in the bill text (unlike MCDPA’s exemptions for GLBA/FCRA-regulated financial data or certain banks/credit unions, which do not cleanly cover standalone LPR plate scans).

The Bottom Line

From the repossession industry’s perspective: HF3856 would impose heavy operational, cost, and compliance burdens while offering no carve-outs or alternatives. It would make LPR, a core, efficient tool for locating collateral, largely unusable in Minnesota without costly per-vehicle court orders or impractical signage.

There are broader constitutional red flags. Requiring court orders or warrants for basic location data arguably impairs contractual security interests and raises questions under the Contracts Clause and due-process protections. Out-of-state LPR providers serving Minnesota clients could also challenge the law on Commerce Clause grounds. Violations would expose operators to Minnesota Attorney General enforcement actions and potential MCDPA-level penalties, with no private right of action to defend against, but plenty of risk for civil or administrative headaches.

As of today, the bill remains in committee with no hearings scheduled, but recent media coverage and ACLU backing suggests momentum is building. Repo associations, towing groups, and lender representatives have a narrow window to push for targeted exemptions during testimony, carve-outs that recognize LPR’s role in efficient, peaceful collateral recovery and protect the self-help rights baked into UCC law.

The repossession community cannot afford to sit this one out. Operators who have built business models around LPR are already modeling worst-case scenarios: higher fees passed to lenders, reduced recovery rates, and possible market exits for smaller Minnesota firms.

Kevin Armstrong

Publisher

LPR Repo Data Gathering and Use Under Fire in MN Bill – LPR Repo Data Gathering and Use Under Fire in MN Bill – LPR Repo Data Gathering and Use Under Fire in MN Bill

LPR Repo Data Gathering and Use Under Fire in MN Bill – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Compliance – Police – LPR

More Stories

Repo Chase Leads to Gunfire in Miami Gardens

Repossessed Vehicle Stolen from Lot – El Paso Man Arrested

Equifax Report Signals Auto Credit Stress Remains Elevated Despite Signs of Stabilization

Arkansas Tow Company Owner Charged in Alleged Fake Repossession Scheme

Former Tricolor COO Pleads Guilty as Bankruptcy Fallout Continues to Impact Repossession Industry

Alleged Armed Repo Agent Arrested After Chase and Pit Maneuver During Repossession Attempt