Why repossession volume still isn’t telling the whole story

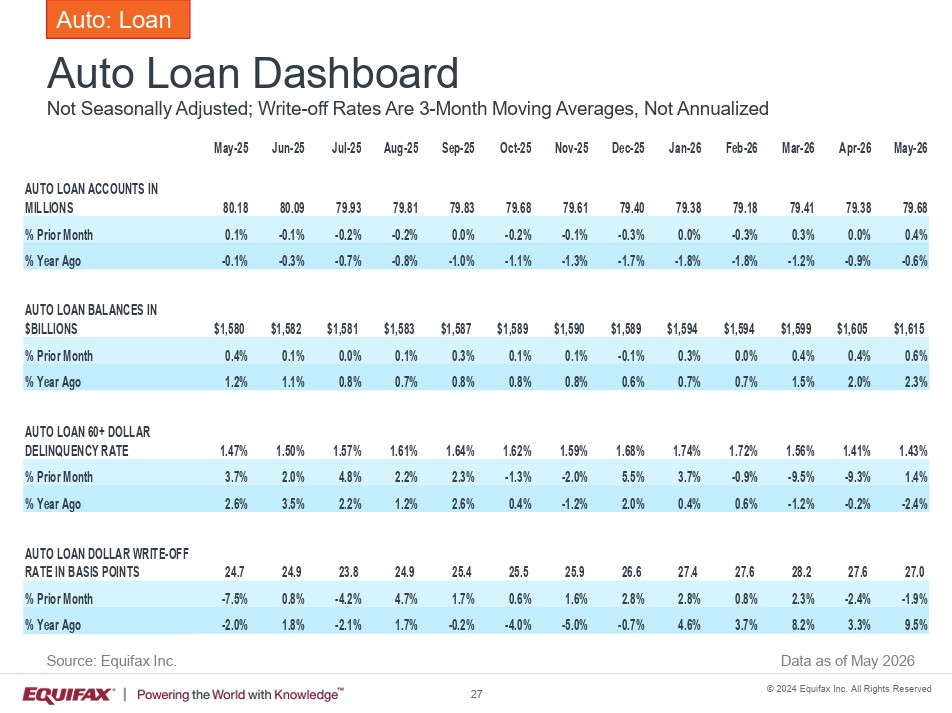

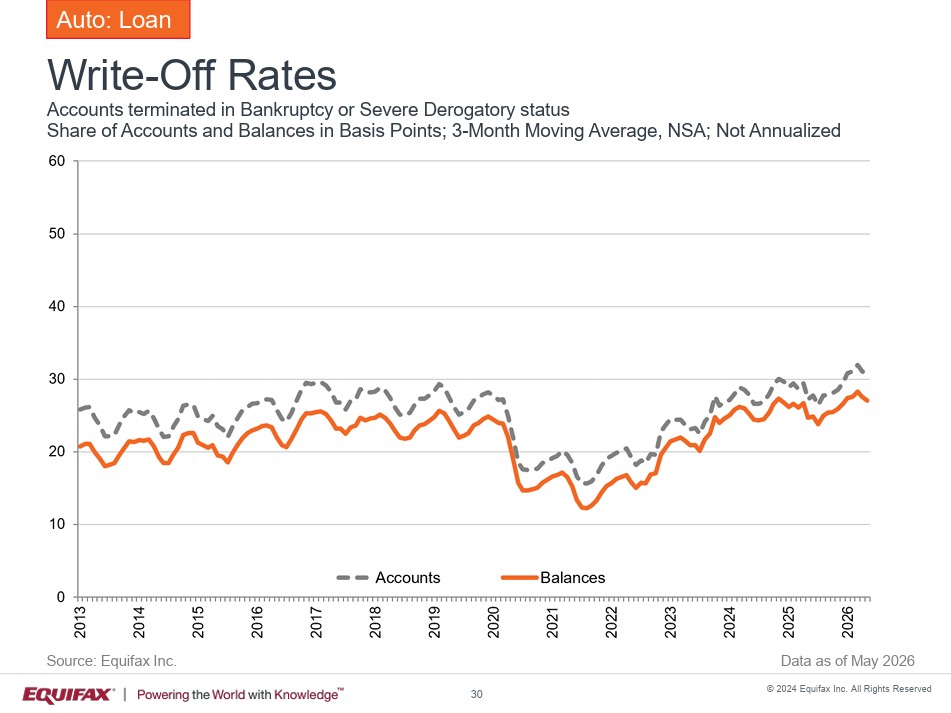

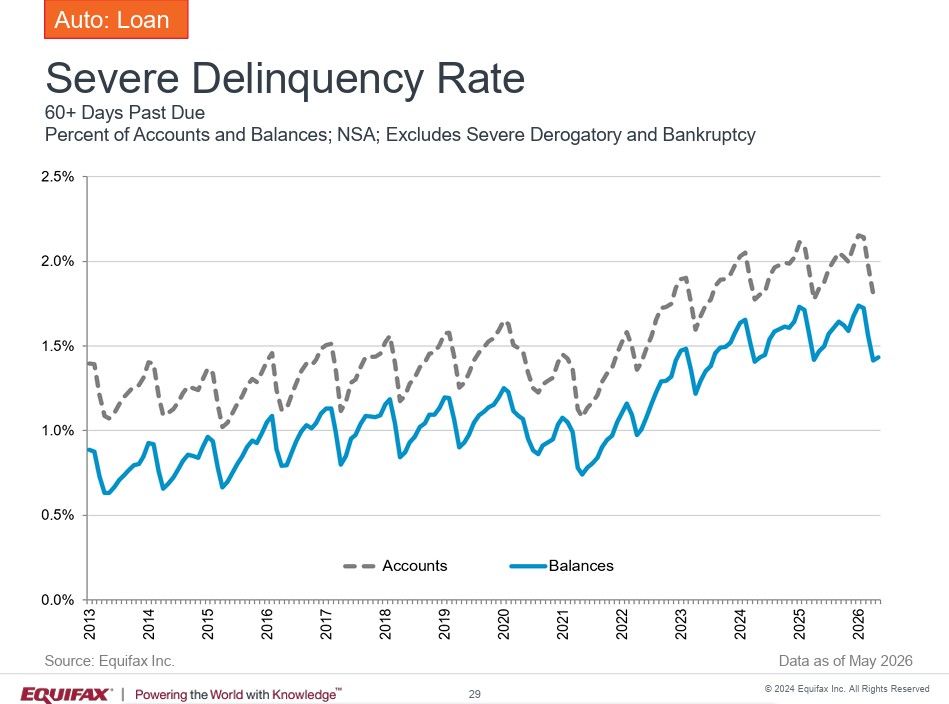

The latest National Consumer Credit Trends Report from Equifax paints a familiar picture of today’s auto finance market: delinquencies remain well above historical norms, consumers continue carrying record debt burdens, and lenders are relying on increasingly creative strategies to keep troubled loans from becoming losses.

Yet one statistic is missing from the discussion: repossessions.

For recovery agencies across the country, that omission highlights one of the most unusual developments in modern auto finance. Delinquencies remain elevated, but repossession assignments have not increased to the degree historical models would have predicted.

For an industry that has long viewed delinquency as the leading indicator of repossession volume, today’s market is challenging one of its oldest assumptions.

The question isn’t whether borrowers are struggling.

The question is what lenders are doing differently once they fall behind.

Read The Entire Equifax Report Here!

A New Era of Loss Mitigation

For decades, the progression of an auto loan was fairly predictable. A borrower missed payments. Collection efforts intensified. If those efforts failed, the account was assigned for repossession.

Facing a combination of pandemic-era servicing changes, regulatory scrutiny, higher vehicle prices, affordability concerns, and rising recovery costs, lenders now have a much larger toolbox before authorizing repossession.

Rather than immediately assigning an account for recovery, they increasingly have options such as:

- Payment extensions

- Deferred payments

- Loan modifications

- Term extensions

- Temporary hardship programs

- Interest adjustments

- Internal repayment agreements

Every one of those options delays, or sometimes completely avoids, a repossession assignment.

For consumers facing temporary financial hardship, these programs can provide valuable breathing room. For lenders, they postpone the recognition of losses while preserving customer relationships.

For repossession agencies, however, they also reduce assignment volume despite continued deterioration within loan portfolios.

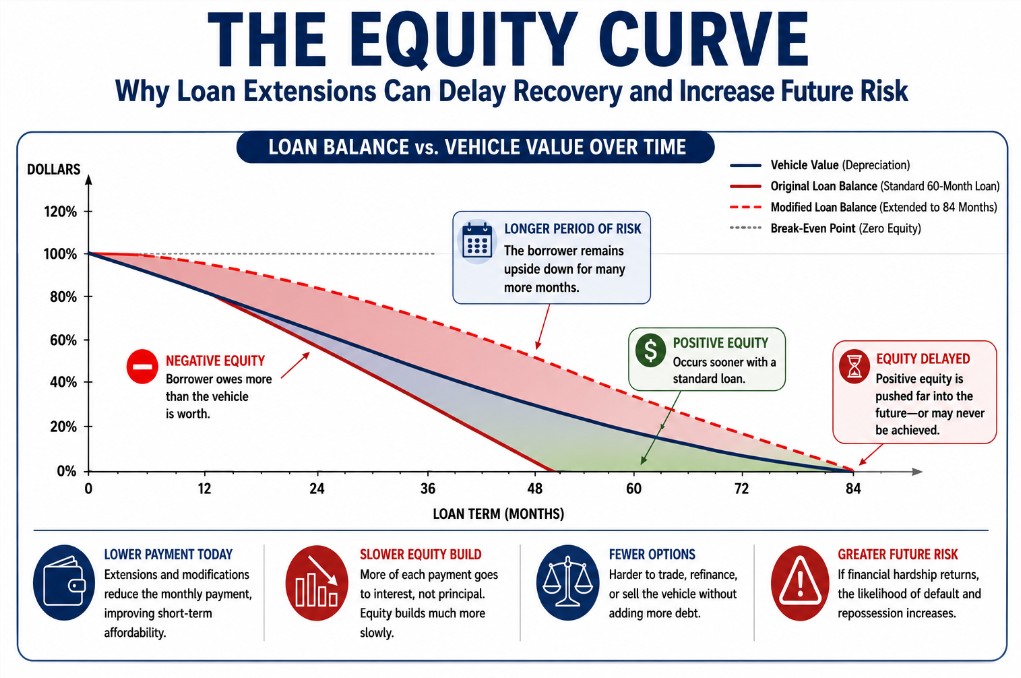

Longer Loans Are Buying Time

Longer loan terms have quietly become one of the industry’s primary loss-mitigation tools.

Sixty-month loans were once the standard. Today, 72-month contracts are common, 78-month financing continues to grow, and 84-month terms are no longer unusual. Loan modifications often extend repayment even further.

The lower payment may improve affordability, but it rarely reduces the amount owed.

Instead, it buys time.

Borrowers who remain current after receiving a modification still carry the same underlying debt burden, often for years longer than originally anticipated. In effect, time itself has become another financing tool.

The Hidden Cost of “Extend and Pretend”

Loan modifications and term extensions may reduce a borrower’s monthly payment, but they rarely improve the underlying economics of the loan.

In many cases, extending repayment simply slows the rate at which principal is paid down while the vehicle continues to depreciate. The result is a longer period of negative equity, leaving borrowers owing substantially more than their vehicle is worth for a greater portion of the loan’s life.

That has implications beyond the lender’s balance sheet.

Borrowers trapped in long-term negative equity often have fewer options when their financial circumstances change. Trading into another vehicle becomes more difficult without rolling unpaid debt into a new loan. Selling the vehicle may no longer generate enough proceeds to satisfy the outstanding balance.

Even borrowers who continue making payments may begin to view the vehicle less as an asset and more as a financial obligation they cannot easily escape.

Behavioral economists have long noted that people become less committed to investments they perceive as offering little chance of improving their financial position. While many modified loans ultimately perform successfully, prolonged negative equity can erode a borrower’s incentive to continue investing in a vehicle they no longer believe has meaningful value.

We all saw this happen before to the real estate market during the Great Recession.

For lenders, loan modifications may provide valuable time for borrowers experiencing temporary hardship. But if extensions merely postpone repayment while allowing loan-to-value ratios to deteriorate further, today’s successful workout could become tomorrow’s larger loss.

Delinquency Doesn’t Always Mean Default

Historically, serious delinquency was one of the strongest predictors of future repossession.

That relationship has weakened.

Today’s servicing environment has created a growing gap between delinquency statistics and actual defaults. Many delinquent borrowers eventually become current again through modifications or repayment plans. Others remain delinquent for considerably longer before lenders determine whether repossession is economically justified.

The result is that delinquency has become a less reliable predictor of immediate recovery activity than it once was.

The Hidden Pipeline

That does not necessarily mean credit risk is improving. Instead, it may indicate that lenders are carrying a growing inventory of distressed loans that have not yet reached final resolution.

Some borrowers will successfully work through temporary hardship. Others eventually will not.

The industry’s challenge is determining how many of today’s modified loans represent genuine recoveries, and how many simply postpone inevitable defaults.

For repossession agencies attempting to forecast future assignment volume, that distinction matters enormously.

Looking Beyond Delinquencies

The Equifax report confirms that financial stress remains widespread across American households. But perhaps the most important takeaway isn’t what the report says.

It’s what traditional credit metrics no longer fully explain.

Delinquencies remain elevated. Debt continues to grow. Yet repossession activity is increasingly influenced by lender strategy as much as borrower behavior.

For recovery agencies, that means assignment volume has become a lagging indicator rather than a direct reflection of consumer financial health.

Understanding today’s repossession market requires looking beyond delinquency rates alone. Loan modifications, extended repayment terms, servicing philosophy, recovery costs, vehicle values, and regulatory considerations have all become part of the equation.

As lenders continue adapting to today’s credit environment, recovery professionals may find themselves watching lender behavior as closely as borrower behavior.

The next wave of repossessions may not be determined solely by delinquency rates, but by the point at which lenders decide temporary relief has run its course and losses can no longer be deferred.

Equifax Report Signals Auto Credit Stress Remains Elevated Despite Signs of Stabilization – Equifax Report Signals Auto Credit Stress Remains Elevated Despite Signs of Stabilization – Equifax Report Signals Auto Credit Stress Remains Elevated Despite Signs of Stabilization

Read The Entire Equifax Report Here!

Equifax Report Signals Auto Credit Stress Remains Elevated Despite Signs of Stabilization – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Lending – Auto Loan – Delinquency – Equifax

More Stories

Attempted Murder Charge Moves Forward Against Memphis Repossessor

Federal Reserve Data Exposes the Other Repossession Industry

California Appeals Court Hands Major Victory to DRN in Landmark LPR Case

Recovery Agent Attacked During Stockton Repossession Attempt

Dealer Accused of Driving Away During Repo with Recovery Agent Beneath Vehicle

Charlotte Tow Owner Faces Felony Charges Over Repo Attempt