The Risk Doesn’t Reset. It Accumulates

GUEST EDITORIAL

After a phone call with a dear business associate, I found myself reflecting on a question that I believe deserves more discussion within our industry. How many times should the same vehicle be repossessed?

As repossession agents, we don’t make lending decisions. We don’t determine whether a loan should be reinstated. We don’t decide whether another repossession assignment should be issued.

Our responsibility is to receive a lawful assignment and perform our job professionally, legally, and safely.

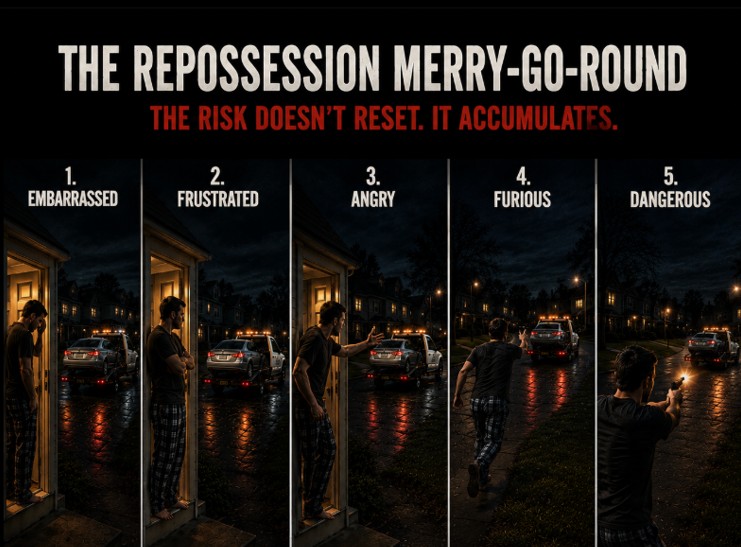

Yet more and more, we’re seeing the same vehicles, and the same consumers, come across our desks multiple times throughout the life of a single loan. Sometimes we don’t even realize it until the consumer says, “This is the third (or fourth) time my vehicle has been repossessed.”

First repossession

Second repossession

Third repossession

Sometimes even a fourth.

With every assignment comes another opportunity for confrontation. Another chance for allegations of property damage. Another wrongful repossession claim. Another insurance exposure. Another lawsuit.

What many outside our industry don’t realize is that most repossession companies are small, family-owned businesses. We invest heavily in licensing, insurance, compliance, employee training, equipment, and technology.

Every assignment we accept carries significant operational and legal risk, and we perform our work in good faith based on the lender’s authorization that the account is legally eligible for recovery.

This isn’t about questioning a lender’s legal right to repossess collateral when a borrower is in default. That right exists.

The question is whether repeated repossession assignments should trigger a higher level of review before another independent contractor is sent into the field.

Should there be additional oversight before a third or fourth repossession is authorized?

Should lenders evaluate whether repeated reinstatements are actually benefiting the consumer, or simply repeating the same cycle?

Should the party authorizing repeated repossessions bear more responsibility for the risks created by those decisions?

These aren’t accusations. They’re honest questions from an industry that assumes substantial risk every time we accept an assignment.

How many repossessions on the same loan are too many?

The Repossession Merry-Go-Round – The Repossession Merry-Go-Round – The Repossession Merry-Go-Round

Respectfully,

Stephanie Findley

CEO,

I R Services

The Repossession Merry-Go-Round – Lawsuit – Lawsuit – Lending – Auto Loan – Repossession Violence – Repossession History – Repossession – Repossess – Repossession – Repossession Agency – Repossessor

More Stories

Repo Agent vs. Repo Agent – The Battles in the Field

The Forwarding Generation and the Value of a Box of Donuts

When Fear Turns Violent: Understanding the Psychology Behind Repossession Confrontations

Bridgecrest’s Fuel Surcharge Program a Step Forward—But Is It Enough for California?

The New Yorker Article – The Story She Didn’t Write

The Registration Gap: A Compliance Brief for Repossession Industry Stakeholders