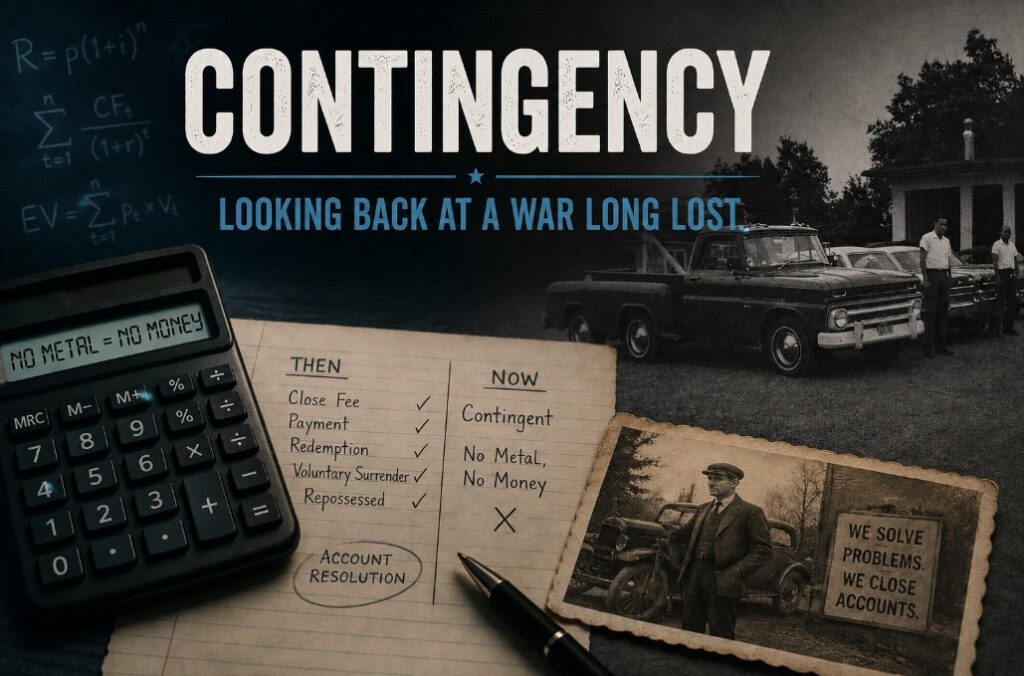

The Economics That Changed an Industry

EDITORIAL

I was recently doing some clean up on the CUCollector site and stumbled across an old editorial from 2018 titled “The Stupid Math behind Contingent Repossession Assignments“. It’s an old argument from an era when the war against contingent repossession assignments was already losing, but it’s an interesting glimpse of an era long gone and illuminates just how the repo industry got where it is.

The Stupid Math behind Contingent Repossession Assignments

“People don’t always respond to incentives in the ways you might predict. What distinguishes good economic thinking from bad is recognition of the subtle, creative, and often unforeseen ways that people respond to incentives.” Economist Glen Whitman

GUEST EDITORIAL

Ask any economist, and he’s tell you that the business world works best where there are proper incentives in place to guarantee the best performance. And bad incentives produce what’s called “perverse consequences”. And there’s a secret perverse consequence to contingency assignments that’s being kept hidden.

One of the really dumb things about assigning (or working) repossession accounts on a contingent basis is that it doesn’t incentivize intelligent field work. In a world where it’s “no metal/no money”, ignorance is bliss on the other half of the assignments that don’t get picked up. Millions of dollars worth of collateral lost because no one is offering to pay for golden information that the recovery agent could gather. The creditors THINK they are getting this information, but they aren’t.

And tens of millions of dollars of recoverable collateral are being lost every year. Beating the repossessor out of $150, to lose a $10,000 car, doesn’t make any sense…and multiply that by tens- or hundreds of thousands.

Go to any repossession convention and sit around the table and talk with a repossessor who accept contingent work. “Yeah, the work sucks, but I only hit it when I am in the area. I make up the updates, don’t run any database searches, and don’t contact any neighbors or occupants. Why should I? It just doesn’t pay. If the car is there, I get it, but that’s all”. In fact, there is a “perverse incentive” to NEVER make contact, because it could scare off the customer, with the repossessor being then rewarded with a big goose-egg. Better just to drive by, and then only when it’s convenient.

As a result, the recovery ratios are LOWER on contingent assignments nationwide, often by MORE than 20%-30%.

One representative for a forwarding company reported that they knew that they were getting lower numbers, but by bouncing the account from agent to agent, they eventually could reach the magic 65% recovery ratio that is often held out as a good number (the other 35% could be charge-offs, but they could be positive resolutions too).

If a client or a forwarder is not getting a 60-70+% repossession rate on their portfolio, they need to really research why not. Either their accounts are in really, really bad, or their incentive program for their repossession agents does not encourage their best efforts. And our industry, as a whole, knows which one is the problem.

If I were on the board of directors of a big lender, if I learned that 30% of my cars needlessly went into charge-off because of a lame, short-sighted vendor incentive plan, I’d be outraged. These creditors or forwarders who think they are beating the repo industry into submission using these poorly-constructed incentives are eventually going to wake up and realize that lowering repossession expenses are only exponentially skyrocketing charge-offs and litigation expenses.

Patrick Altes

Falcon International

FOMO

Patrick was spot on. But here we sit eight and a half years later, and no one even talks about it anymore. Why?

Because the war is lost. Why?

Because the repo industry let it happen to itself. Why?

FOMO. Fear of missing out. A pervasive attitude of “If I don’t do it, someone else will.”

Fast forward a couple of years and it only got worse.

Personal property fees, gone. Storage fees, gone. Mileage, gone.

On top of this, the repossession fees remained stagnant and continue to properly address inflation and increased costs of operations. Basic economics became merely a quiet grumble that few could dig in their heels on and even more feared angering the lenders and forwarders by demanding more.

The Forgotten Basics

Somewhere along the way, the repossession industry stopped talking about economics and started talking only about price.

Those are two very different conversations.

For much of the industry’s history, from the 1920s through the latter part of the twentieth century, a repossession assignment wasn’t judged solely by whether the vehicle ended up on the back of a tow truck. Agencies were paid close fees when they resolved the account, whether that meant recovering the collateral or motivating the borrower to bring the loan current, redeem the vehicle, or otherwise satisfy the lender’s objective.

The recovery agent’s job wasn’t simply to find cars. It was to solve problems.

That incentive rewarded investigation, persistence, communication, and intelligence gathering. Every contact with a borrower or neighbor, every updated phone number, every employment lead, every confirmed address, every piece of field intelligence had value because it increased the likelihood of an account resolution.

For all intents and purposes, contingency assignments killed account resolution almost overnight.

Once compensation became “no metal, no money,” the industry’s incentive shifted from resolving accounts to chasing only the recoveries with the highest probability of success. Information that once had real economic value suddenly became uncompensated labor.

The result wasn’t that recovery agents became less professional.

The incentive to perform the additional work simply disappeared.

Economists call that a perverse incentive.

Looking back, contingency assignments didn’t simply eliminate close fees. They eliminated an entire incentive system that had existed for generations. For nearly a century, agencies were rewarded for creating account resolutions. Today, they’re largely rewarded only for creating repossessions.

That distinction may seem subtle.

In reality, it changed the economics of an entire industry.

Thinking back on Patrick’s old editorial, I’m coming to see that the math was never stupid. People simply stopped doing it.

History has a way of becoming invisible. Those who entered the industry after contingency assignments became the norm assume this is how repossession has always worked. It isn’t.

The industry didn’t evolve into this model, it chose it. And every incentive chosen eventually shapes the outcomes one gets.

Contingency – Looking Back at A War Long Lost – Contingency – Looking Back at A War Long Lost – Contingency – Looking Back at A War Long Lost

Kevin Armstrong

Publisher

Contingency – Looking Back at A War Long Lost – Contract – Forwarder – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Repossession History – Auto Loan – Lending

More Stories

Every Recovery Agency Is Also a Lender

The Repossession Merry-Go-Round

Repo Agent vs. Repo Agent – The Battles in the Field

The Forwarding Generation and the Value of a Box of Donuts

When Fear Turns Violent: Understanding the Psychology Behind Repossession Confrontations

Bridgecrest’s Fuel Surcharge Program a Step Forward—But Is It Enough for California?