Why Repo Volume Is Dropping and What Comes Next

Across the country, a growing number of repossession agencies are reporting the same thing: assignment volumes are down, and not in the way we typically expect this time of year. Additional data provided by Recovery Database Network (RDN) to members of the State Repossession Associations confirms the same. While seasonal slowdowns around tax time are nothing new, this dip feels sharper, less predictable, and disconnected from the patterns we’ve seen in both pre- and post-pandemic cycles.

The question on everyone’s mind is simple:

Is this temporary, or is something bigger changing?

A Market Shift, Not Just a Seasonal Dip

At first glance, the explanation may seem straightforward. Tax refunds are hitting accounts, borrowers are catching up, and delinquencies are temporarily curing. That’s part of the story, but it’s not the whole story.

At first glance, the explanation may seem straightforward. Tax refunds are hitting accounts, borrowers are catching up, and delinquencies are temporarily curing. That’s part of the story, but it’s not the whole story.

What we’re seeing is a shift in lender behavior.

Today’s lenders are:

- Extending repo triggers further out – 90 days out from 60 days out

- Increasing the use of payment arrangements and deferrals – Extend and pretend

- Leveraging data to identify accounts likely to cure – Fortune telling

- Pushing harder to resolve accounts before repossession assignments

At the same time, rising losses and operational costs are forcing lenders to ask a more direct question:

“Does this vehicle justify the cost and risk of recovery?”

In many cases, the answer is increasingly no, at least not yet.

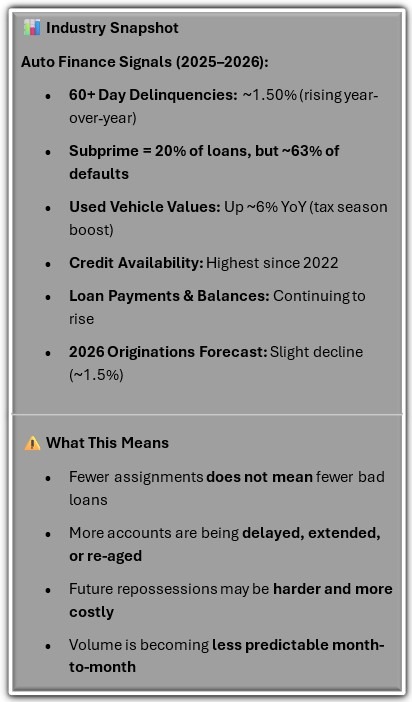

Why Volume Feels Artificially Low

Several forces are converging to suppress assignment flow:

- Tax Season Effects: Borrowers are using refunds to temporarily stabilize accounts

- Delayed Defaults: Accounts that would have been assigned are being extended or re-aged

- Portfolio Cleanup: Legacy “dead” accounts are being written off instead of recycled from forwarder to forwarder and agent to agent in endless cycles of assignment

- Selective Placement: Lower-value units are less likely to be assigned at all

The result is not necessarily fewer problem loans, but rather fewer immediate repossession opportunities.

What Comes Next: A Likely Rebound, With a Catch

While current volumes may feel concerning, the underlying risk in the system has not disappeared. In fact, many indicators suggest it has simply been delayed.

As we move beyond the tax season window, agencies should prepare for:

- A return of assignments in late Q2 and Q3

- More difficult recoveries (longer delinquency cycles, harder-to-find units)

- Increased operational cost per recovery

- Greater volatility in monthly volume

In short, the industry may not be heading into a prolonged slowdown, but rather into a more uneven and less predictable cycle.

A Changing Repo Landscape

For years, the repossession industry has operated within a relatively reliable rhythm. That rhythm is changing.

We are moving toward a model where:

- Volume is less consistent

- Assignments are more selective

- Recoveries are more complex

- Margins are under greater pressure

For lenders and forwarders, this evolution represents a shift toward efficiency and risk management.

For agents, it represents a need to adapt quickly, or fall behind.

The Risk No One Talks About

During slow periods, agencies often feel pressure to replace lost volume quickly. That can lead to:

- Signing clients with unfavorable terms

- Accepting lower fees

- Taking on higher-risk or poorly managed portfolios

This is where long-term damage is done.

Not all volume is good volume.

And in a tightening environment, bad volume can be more costly than no volume at all.

The Path Forward

This moment calls for discipline across the industry.

For agents:

- Focus on operational efficiency over raw volume

- Protect margins and client quality

- Prepare for volatility, not stability

For lenders and forwarders:

- Maintain strong partnerships with proven agents

- Recognize the rising cost of recovery operations

- Understand that delayed assignments often become more difficult and expensive

Final Thought

What we are experiencing may not be a slowdown, it may be a recalibration.

The accounts are still out there.

The risk is still present.

But the timing, the strategy, and the economics of repossession are changing.

Those who recognize and adapt to that shift will be positioned not just to survive, but to lead, in the next phase of the industry.

Kevin Armstrong

Publisher

The Repo Slowdown No One Expected – The Repo Slowdown No One Expected – The Repo Slowdown No One Expected

The Repo Slowdown No One Expected – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Fuel Costs – Gas Prices – Forwarder – Subprime Auto Loans – Subprime Auto Loans – RDN – Recovery Database Network – Lending – Auto Loan

More Stories

From Coastlines to Crossroads: CURepo Directory Is Growing! Is Your Agency In?

Trial Date Set for Jayson Click Repossession Murder

Kentucky Bill Seriously Threatens LPR Data Access for the Repossession Industry

Wrongful Death Lawsuit Over 2023 Repossession Shooting Dismissed

Close Call in Detroit: Toddler Left in Repossessed Vehicle, Safely Returned

Razzberry’s Repo Runaway Spawns Auto Theft Charges