…many fee models no longer accurately reflect the actual economics of modern repossession operations.

EDITORIAL

There is a conversation the repossession industry has largely avoided since 1981. Not because it disappeared. Not because the problem was solved. But because the industry was taught to fear discussing it.

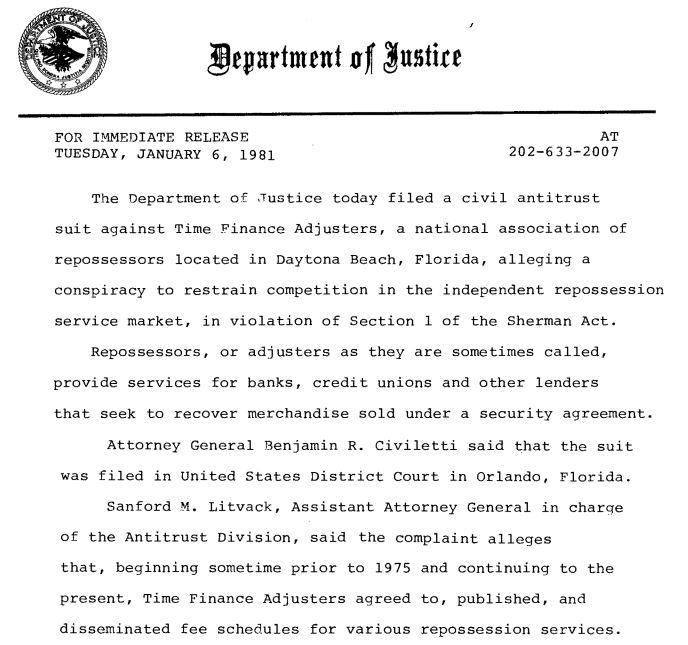

In January of 1981, the Department of Justice filed antitrust actions involving all four repossession industry associations over alleged efforts to standardize fees and restrict competition. The complaint alleged that repossession associations had agreed to and disseminated fee schedules for recovery services, something federal regulators viewed as restraint of trade under the Sherman Act.

Whether one agrees with the government’s position or not, the impact on the industry was undeniable. The repossession world became extraordinarily cautious about discussing pricing in almost any organized fashion. And for the next four and a half decades, something remarkable happened:

The cost of repossession operations continued climbing dramatically…

while recovery fees in many markets barely moved at all.

Think about that for a moment.

The Industry That Time Forgot

Since 1981:

- Fuel prices have multiplied several times over

- Insurance costs have exploded

- Compliance requirements became exponentially more complex

- Labor costs increased

- Vehicle technology evolved dramatically

- Skip tracing changed entirely

- LPR systems became standard operational infrastructure

- Litigation exposure expanded

- Free storage requirements increased

- Cybersecurity risks emerged

- Trucks became vastly more expensive

- Licensing and regulatory burdens intensified

Yet in many areas of the country, repossession fees still resemble structures established decades ago under entirely different economic realities.

The industry adapted operationally. But economically, many agencies remained frozen in time.

That disconnect is becoming impossible to ignore.

Today, fuel prices are once again placing enormous pressure on recovery agencies nationwide. Diesel volatility alone is reshaping operational decisions. Agencies are reducing coverage areas, limiting speculative sweeps, consolidating field operations, and reevaluating assignment acceptance based on economics rather than simply volume.

And frankly, many operators are quietly asking a question the industry has avoided for years:

How did we get here?

Bound to the Past

Part of the answer may be psychological.

The 1981 antitrust actions created a lasting industry culture where many agencies became hesitant to discuss pricing pressures publicly at all. Associations became cautious. Operators became fragmented.

Clients became accustomed to static pricing models. Over time, “keeping the client happy” often became more important than understanding whether the work itself remained economically sustainable.

Meanwhile, competition intensified.

And unlike many industries, repossession developed a culture where someone was almost always willing to do the work cheaper. Sometimes far cheaper.

Even if it meant operating on razor-thin margins. Or no margins at all.

The result is an industry that has become extraordinarily resilient operationally, but often fragile economically.

That is not sustainable forever.

Now to be absolutely clear: there is a very important distinction between illegal price fixing and legitimate economic discussion.

Adult Conversations

The industry does not need standardized pricing agreements to have honest adult conversations about operational realities.

Those are two very different things.

- Truckers discuss fuel costs.

- Contractors discuss labor shortages.

- Healthcare systems discuss reimbursement pressures.

- Agricultural groups discuss equipment inflation.

Industries are allowed to discuss economics.

What they cannot do is collectively agree on pricing.

That distinction matters.

The repossession industry absolutely can, and probably should, be more adamant and persuasive in educating lenders, forwarders, and clients about what modern recovery operations actually cost in 2026.

Because many outside the industry simply do not seem to fully understand what recovery agencies now absorb operationally:

- Fuel volatility

- Compliance infrastructure

- Insurance escalation

- Technology investments

- Litigation exposure

- Labor shortages

- Increasing violence and risk

- Data security obligations

- Multi-camera systems

- Storage liabilities

- Fleet maintenance inflation

These are not theoretical concerns. They are daily operational realities.

The larger issue may not even be fuel itself.

Reflections of Actuality

Fuel is simply exposing the underlying structural weakness that has existed for years:

many fee models no longer accurately reflect the actual economics of modern repossession operations.

And eventually, markets correct unsustainable conditions.

The correction may not come through organized fee increases. It may come through shrinking capacity.

- Fewer agencies.

- Reduced rural coverage.

- Longer response times.

- Less experienced operators.

- Reduced urban coverage.

- More consolidation.

- Less investment in compliance and technology.

Those outcomes are not hypothetical anymore. Some are already beginning to appear.

The agencies most likely to survive long term will probably be the ones that become more disciplined about understanding true operational costs and making economically rational decisions, even when those decisions are uncomfortable.

That may mean declining unprofitable work, reducing service areas, reevaluating staffing models, diversifying revenue streams or having difficult conversations with clients about sustainability.

Because at the end of the day, repossession is not simply a service business. It is infrastructure.

And infrastructure eventually breaks when economics no longer support maintenance.

The Sin of Silence

For decades, the repossession industry has absorbed increasing operational pressure largely in silence.

But silence does not stop inflation.

Silence does not lower fuel prices.

Silence does not reduce insurance premiums.

Silence does not recruit field operators.

Silence does not replace worn-out trucks.

The industry does not need collusion. It does not need coordinated pricing. And it certainly does not need antitrust problems.

But it does need honest economic transparency. Because the cost of recovery has changed dramatically.

And pretending otherwise is becoming harder with every mile driven.

Kevin Armstrong

Publisher

The Conversation the Repossession Industry Has Avoided for 45 Years – The Conversation the Repossession Industry Has Avoided for 45 Years – The Conversation the Repossession Industry Has Avoided for 45 Years

The Conversation the Repossession Industry Has Avoided for 45 Years – Repossession Violence – Repossession History – Repossession – Repossess – Repossession – Repossession Agency – Repossessor – LPR – Compliance – Forwarder

More Stories

Auto Credit Is Flowing Again. So Is Future Repo Risk

Think Before You Post – Your Business Depends on It

When the Lender Runs Out of Road: Why Car-Mart’s Problems Could Become Yours

The Growing Insurance Crisis Threatening the Repossession Industry

Why Did I Get Out of the Repossession Business?

Contingency – Looking Back at A War Long Lost