New York, NY – 6 April 2018 – Growing numbers of small subprime auto lenders are closing or shutting down after loan losses and slim margins spur banks and private equity owners to cut off funding.

Summit Financial Corp., a Plantation, Florida-based subprime car finance company, filed for bankruptcy late last month after lenders including Bank of America Corp. said it had misreported losses from soured loans. And a creditor to Spring Tree Lending, an Atlanta-based subprime auto lender, filed to force the company into bankruptcy last week, after a separate group of investors accused the company of fraud.

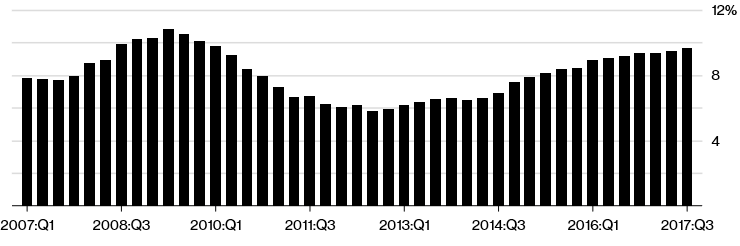

Delinquencies Driving Higher

Non-bank lenders’ subprime auto loans are going bad at the highest rate since 2010.

Source: New York Fed Consumer Credit Panel/Equifax

The pain among smaller lenders has parallels with the subprime mortgage crisis last decade, when the demise of finance companies like Ownit Mortgage and Sebring Capital Partners were a harbinger that bigger losses for the financial system were coming. In both cases, rising interest rates helped trigger more loan losses.

“There’s been a lot of generosity and not a lot of discretion on the part of lenders and investors,” said Chris Gillock, a banker at Colonnade Advisors, which advises companies on subprime auto investments. “There’s going to be more capitulation.”

Representatives for Spring Tree didn’t respond to requests for comment. A lawyer for Summit said “restructuring in a Chapter 11 bankruptcy proceeding is the best strategy to ensure its long term success” and the company is working with its vendors and lenders to meet its obligations.

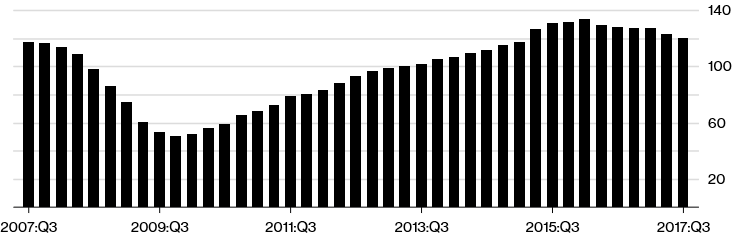

Different Cycle

This time around, the financial system’s losses are expected to be much more manageable, because auto lending is a smaller business relative to mortgages, and Wall Street hasn’t packaged as many of the loans into complicated securities and derivatives. As of the end of September, there were about $280 billion of subprime auto loans outstanding, according to the Federal Reserve Bank of New York, compared with around $1.3 trillion in subprime mortgage debt at the start of 2007. There isn’t a standardized definition of subprime borrowers, though it generally encompasses borrowers with FICO credit scores below 600 to 640 on an 850 point scale.

“When you think about the effects of housing versus autos, they’re a lot different,” said Kevin Barker, a stock analyst covering specialty finance companies at Piper Jaffray & Co. Losses tend to be less severe for car loans because they are smaller than mortgages and borrowers pay them down faster, he said, and the collateral is easier to repossess. With home loans, in many states foreclosures require a lengthy court process.

“If you stop making payments on your car for three months, someone can come out to your driveway and take it,” Barker said.

For some money managers and companies, though, losses could still hurt. Private equity firms and other investors have poured billions of dollars into subprime auto lenders, hoping for big profits. But subprime and near-prime auto lending volumes by one measure peaked in the first quarter of 2016 at $134 billion, and has declined every quarter since then, according to New York Fed data. That left companies fighting for fewer loans.

Past Peak Lending?

Finance companies’ lending to less creditworthy borrowers has been declining since 2016.

Source: New York Fed Consumer Credit Panel/Equifax

“There’s been intense competition. The margins just aren’t there,” said Troy Cavallaro, Pelican’s chief executive officer. “We were waiting it out to hopefully see the tides turn. We didn’t see it happen in the timeline we expected.” Pelican’s private equity backer, Flexpoint Ford LLC, stopped funding the company after inking a deal to invest as much as $50 million in 2013. Representatives for the firm didn’t respond to requests for comment.

Years of loose lending have resulted in growing numbers of subprime borrowers falling behind on their bills. In the quarter ended September, 9.7 percent of loans that auto-finance companies made to the riskiest borrowers were overdue by 90 days or more, according to a study last year by the New York Fed. That’s the highest percentage since 2010. The weakness is making it more expensive for some subprime auto lenders to package loans into bonds, though none of the companies that recently closed or filed for bankruptcy have issued such securities.

Easy Money

It’s a cycle the subprime auto industry has seen before. From 1997 to 1999, 41 lenders filed for bankruptcy, shut down or were acquired as losses from bad loans piled up, according to Moody’s Investors Service. For this cycle, easy money may have spurred lenders to be looser in their underwriting or fail to properly vet borrowers’ incomes, said Colonnade’s Gillock. In Summit’s bankruptcy documents, lender Bank of America said the company had repossessed and sold millions of dollars worth of cars without writing down the loans. The move allowed the company to hide operating losses and borrow more money to fund loans, the bank said. Summit for its part said in court documents that it was forced to file for bankruptcy after delinquencies rose following Hurricane Irma.

With Spring Tree, an investor said he had loaned $300,000 to the company in 2015 with the understanding that his money would be fully secured and would be the first to get paid back if borrowers on auto loans defaulted. In a lawsuit filed in November, the investor said he had been defrauded. In March, a separate investor filed to put the lender into involuntary bankruptcy.

“This industry goes through cycles,” said John Anglim, a senior director in the consumer ABS group at S&P Global Ratings. He said subprime auto lenders that issue ABS broadly look healthy. “The cycle right now is that there’s a bit of tightening.”

Source: Bloomberg

Small Subprime Lenders Are Starting to Fail – Delinquency – Repossession

More Stories

A Step Toward Safer Repossessions: PAR’s Field Protection Program

MN LPR Bill Bites the Dust

Bat-Wielding Repo Rampage Ends in Prison Sentence

LPR Repo Data Gathering and Use Under Fire in MN Bill

Senator Warren Goes Back Down the Lending and Repossession Rabbit Hole

Repo Industry Pioneer Joe Taylor Passes Away