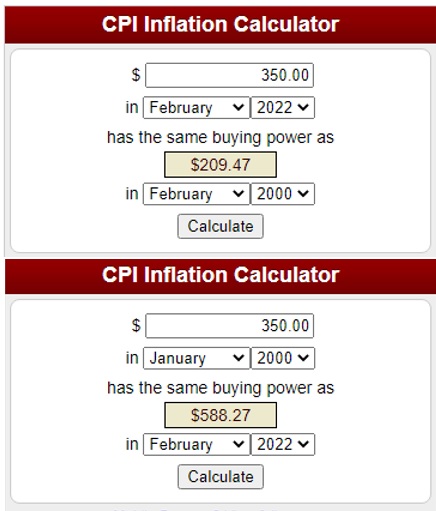

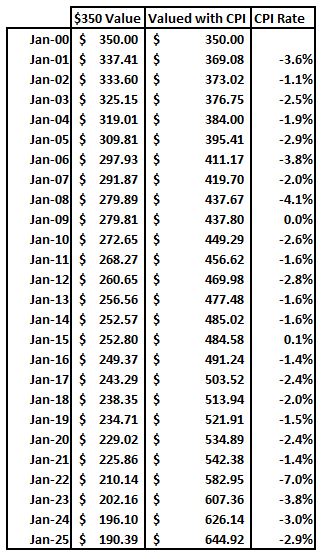

$350 Fee in 2025 = $190.39 Value in 2000 – Adjusted for Inflation That Fee Would be $644.92 Today

The price of everything goes up over time. Blame a devaluing dollar, cost of operations, goods or taxes, but it is inevitable in everything. Everything that is, except the eternally flat repossession fee. It’s been almost three years since I’ve beaten the dead horse and I guess I’m a little antsy and overdue.

Repossession volume is at record highs and agencies are swamped with work to such a point that recovery turn times are longer than they have been in many years. While some lenders and forwarders have seen the writing on the wall in performance and efficiency and increased what they will pay for repossession fees, some have not. So, there still remain many in the industry still accepting $350 for a repo who may need a reminder of what fees used to look like.

The Big Mac Index and the Repo Fee

Please bear with me. The Big Mac Index is a price index published since 1986 by The Economist as an informal way of measuring the purchasing power parity (PPP) between two currencies and providing a test of the extent to which market exchange rates result in goods costing the same in different countries. It “seeks to make exchange-rate theory a bit more digestible.

But for our purposes, I’m going to use just the gathered price comparison data through the years here in the USA.

The “Big Mac Index” as it is known, states that in 2000, a Big Mac costed on average $2.24, a current value of $4.29. Today, that burger, whose pickles are thicker than the slivers of mystery meat between the buns, costs an average $5.58, a year 2000 value of $2.92.

Doing just a little research, I also found that a delivered Dominos pizza would cost you about $13.00 in the year 2000, a modern equivalent of about $24.88. Fast forward to 2025 and depending on your location, it costs about $21.58. That’s a minor decrease for Dominos, but still a reasonable increase.

Despite the desire to remain competitive and as the result of inflation, as illustrated, the cost of goods and services increases. ALL businesses adjust their pricing to adjust for inflation. That is, except the repossession industry.

CPI

The Consumer Price Index (CPI) is a measurement method maintained by the Bureau of Labor Statistics (BLS) that tracks the average change over time in the prices paid by consumers for a basket of goods and services, such as food, transportation, and housing, reflecting trends in inflation or deflation.

The Consumer Price Index (CPI) is a measurement method maintained by the Bureau of Labor Statistics (BLS) that tracks the average change over time in the prices paid by consumers for a basket of goods and services, such as food, transportation, and housing, reflecting trends in inflation or deflation.

No goods or services are inherently immune to CPI changes, as the index reflects broad price trends across a basket of items, but some, like certain regulated utilities or subsidized healthcare, may experience slower or less direct price changes due to government intervention or fixed pricing structures.

So, by using CPI rates, we can also look back and forth in time to see the comparable values in repossession fees and do our own Big Mac Index on repo fees.

Repo Fees – A Look Back

In the year 2025, a pretty standard repo fee is about $350. Using the CPI calculator, we can see that if repossession fees had risen with the CPI rate beginning in the year 2000 that the current value would be $644.92. Why is the year 2000 so relevant in repo fees? Because agencies are getting paid about the same now as they were 25 years ago. Truth be told, we were getting paid that much in 1990 and with storage and property fees!

Over the history of the industry, there are numerous stories to reflect on what fees were, and they tended to keep up with the CPI. Fair warning, I am re-using old data to illustrate my point. Rather than recasting the 2025 values to these rate quotes, I’m going to stay with the 2022 values, but you will see the changes that were previously in motion.

1926

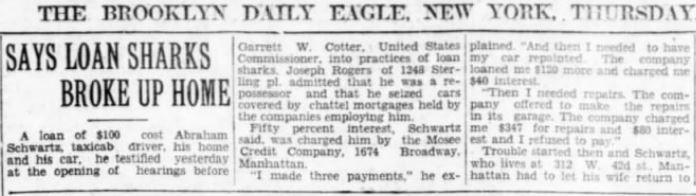

The first known documented public outcry against the repossession process was editorialized. On November 13, 1926, “The Evening Independent” of Massillon, Ohio, reported that three men were held in custody by the local magistrates for being “Loan Sharks” and charged with demanding usurious interest rates. In these hearings, the first known testimony from an unnamed repossessor, states that he was being paid $25 per vehicle for repossessions.

$25 per vehicle = $420.92 – 2022

No insurance. No Trucks and probably no lot. This unknown wildcat agent was doing considerably well considering he likely had little or no overhead.

1949

In a Washington DC Evening Star article titled “We Stole 10,000 Cars“, NAAFA (now AFA) co-founder Ray Barnes, shared several “war stories” from the repossession field. At that time, he claimed to make $35 to $250 per recovery.

$35 to $250 per recovery = $334.09 in 2022 to $3,340 in 2022 value

Again, no insurance and probably one truck used rarely. Storage, property, transport and locksmithing fees on top of that. Ray and Lorna Lou were very hands-on even while operating out of their Flushing, New York office.

Also in 1949

Charles Clark of National Auto Recovery Bureau (NARB) from a March 20, 1949, tell all posted in the Pittsburgh Press, where it is stated “His fee ranges from $10 to $500 depending on the amount of effort involved.”

$10 to $500 = $125.22 to $6,60.76

Once again, no insurance and probably one rarely used tow truck. $10 was probably the price of an intown voluntary. Of course, there were charges for storage, keys, delivery and positive resolution (Closing fees). Yes, closing fees were normal until the 2000’s.

1960

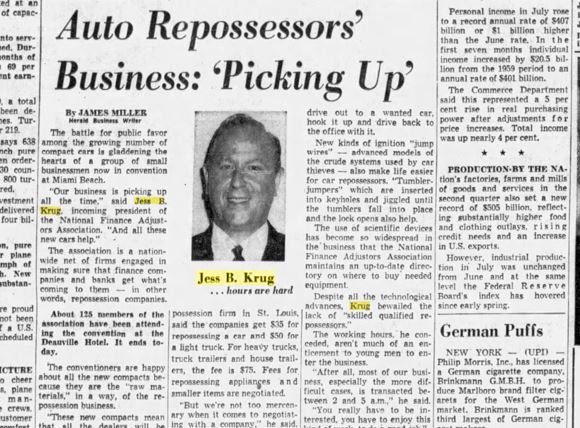

Jess B. Krug, a St. Louis agency owner and then President of the NFA, reported to the Miami Herald member in an article on the National Finance Adjusters meeting at the Deauville Hotel on August 20th – $35 ($352.38 in 2022 currency) cars, $50 ($503.40) for light trucks and $75 ($755.10) for heavy trucks and trailers – August 21, 1960 -The Miami Herald – (Miami, Florida)

These fees were the association set fees and included $.08 cents a mile ($.81 in 2022 value.)

Note: The last three agency owners quoted were members of an association. Associations that provided guidance and uniformity in fees. This is an important detail that I’ll get back to shortly.

1965

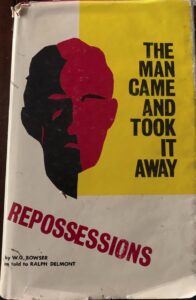

In 1972, veteran repo man from Colorado, Bill “The Cadillac Repo Man” Bowser published “The Man Came and Took it Away.” In this autobiography of his 20 years in the industry he stated that in 1965, he was making $15 a repossession. A book gifted to me by Jeremiah Wheeler. Thanks again Jeremiah!

$15 a repossession = $141.91

Bill owned a small local agency and was in fierce and sometimes violent conflict with his local competitor who used to flaunt Bill’s young criminal record against him to competitors and he claimed would slash tires and damage vehicles to keep his agents from the field. In the book, he stated that “he would raise his fees but was afraid that his competition would benefit from it.”

This fear is one that I was very aware of coming into the business in 1989. Agents were known for slashing each other’s tires and cutting fluid hoses on slide in tow units for similar reasons.

Bill’s book is a great snapshot of the career of a repo man in the 1950s to 1960’s. If you’ve never seen any of it, it’s worth a read.

Click Here!

1978

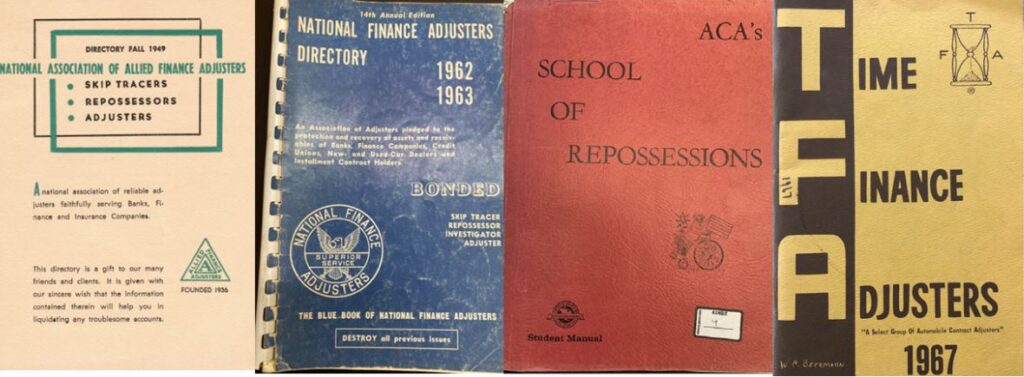

Being in an association before 1980, there were suggested fees posted in the association directories. These directories were issued nationwide to large lists of lenders. The associations themselves published what the suggested fees were so that clients knew what to expect and agency owners maintained some control over their incomes.

Being in an association before 1980, there were suggested fees posted in the association directories. These directories were issued nationwide to large lists of lenders. The associations themselves published what the suggested fees were so that clients knew what to expect and agency owners maintained some control over their incomes.

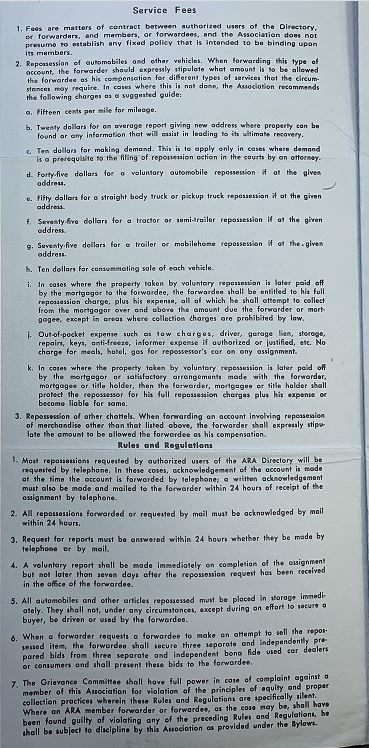

ARA Service Fees Schedule

Fifteen cents per mile. (Don’t laugh, that’s $0.69 in 2022 value)

$20 for developing a new address that results in a recovery. ($91.41)

$10 for making a demand for collateral. ($45.71)

$45 for a Voluntary Repossession ($205.68)

$50 for a truck repossession ($228.54)

$75 for a tractor trailer ($342.81)

$10 for selling repossessed collateral. ($45.71)

While these fees were “suggested”, there were consequences for failing to abide by them.

Keeping Order

Long before the internet, word of mouth and local marketing were the primary way that agencies developed business. That is, unless they could get into one of the then, four associations; the AFA, NFA, TFA or the ARA.

Being a members of one of these associations granted you a place in “The Book” or directories as they were known. These were mailed out cross country and provided that agency owner a secured territory in it. This territorial exclusivity gave them access to lenders their local competition could never have access to.

Up until the 1980’s the repossession associations flourished. Annual conventions were held in places as far away as Hawaii and the Bahamas. Owners made enough money to divest their profits into everything from real estate to auto franchises.

They controlled the fees and the lenders didn’t bat an eye in paying them. The repossession fee was only the vehicle for other fees. Fees, like storage, keys and transport that had very little overhead involved or at least cover most of it.

Of course, the associations kept strict control over the “suggested fees.” Anyone known to breech these covenants was subject to the potential of a typo on their phone numbers or addresses that could rob them of any value to their membership.

And if the threat of losing the value of your place in “the book” wasn’t enough, the association leaders were very influential amongst the member base. Failure to comply with the “suggested fee” program could run you afoul with men such as the NFA’s Frank Mauro of Chicago, a sharp dressed man of six-foot one and 300 pounds or his best friend from Detroit, Art Lamereaux.

And in the TFA, of course there was “The Godfather” Harvey Altes, whose influence spanned across all four associations. And by his side was Chuck Longbardo, an often coarse and vulgar man known to keep a .38 revolver strapped to his ankle and carried a supply of gas cans and road flares kept in the trunk of his car.

When these men suggested something, you listened.

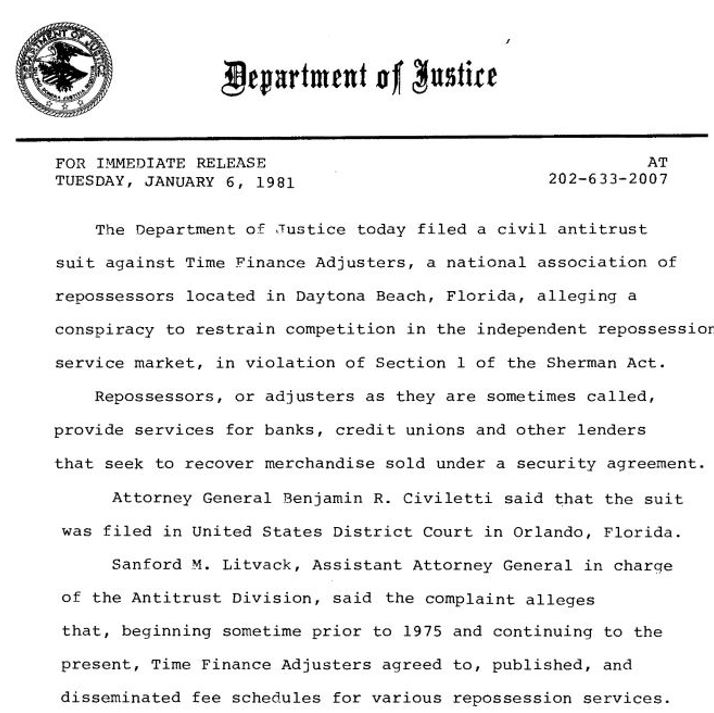

1981

It was all spit and giggles and then, out of left field came the Department of Justice. Stemming from a New Mexico agency owner disgruntled by his inability to join any association, he filed an anti-trust lawsuit against the AFA. This caught attention of the Department of Justice, who on January 5, 1981, filed a charges against all of the national associations for conspiracy to fix prices, restrict territories and limit membership in violation of the Sherman Act, 15 US.

All of the associations paid fines and entered into agreements without an admission of guilt. The agreed upon terms of the settlements were sweeping. No longer could they discuss fees, let alone mandate or “suggest” them. This is why you never hear the national associations speak very loudly about fees. A red line was drawn that they, to this day, dare not cross.

The race to the bottom had only just begun.

1989

This is when I entered the business as a field adjuster for A-1 Adjustment Service, first out of Sacramento, CA under Steve Dove and then back home in Santa Clara, CA under Terry Carter. At this time, the average cost of a repossession was $325, a current value of $781.08, plus storage, keys, delivery, personal property. Of course, we also received closing fees of $75, a current value of $180.25.

1993-1997

I’d worn weary of the field and took a back-office skip tracing job with National Auto recovery Bureau of San Jose, CA (NARB) under longtime NFA member A.M. “Bud” Krohn. NARB was previously owned by Charles Clark mentioned above until Bud bought it in the mid-seventies.

Bud, like most every legitimate agency owner did not work contingent. “Contingent work is for suckers.” He used to say. I finished my time in the repossession industry here as a manager and at that time, the average cost of a repossession was still $325 a current value of $603.45, plus storage, keys, delivery, personal property. Of course, we also received closing fees of $75.

As you can see, the value of $325 dropped in spending power almost $180 in that short span of time. Even then, Bud saw the writing on the wall and complained that the lenders wanted everything for free and was getting ready to leave the business which he finally did about 2004.

I moved on into collections and eventually the credit union world and barely looked at what was going on in the industry for many years. I wanted nothing more to do with being in the business and was content watching it from a safe distance. I never balked at a reasonable increase in repo fees above $325 nor the ancillary fees, but I was unaware of what had been going on in my absence.

2010

Years rolled by when I started CUCollector. I had never intended it to be about repossessions but quickly found myself leaning into it. Especially after learning how prevalent contingency had become and how the forwarding industry had driven a wedge between the agencies, associations and the lenders.

Harvey, Frank, Art and Chuck had all passed away or walked away from the industry. There was no one left to intimidate the association members from drinking from the Guyana Grape flavored cyanide trough of forwarding. And out of a lack of unity or cohesive concerted effort to fight for reasonable fee increases, there were none.

At this time, agencies were barely making $325 a repo, but at least they still got paid some storage and personal property fees. But unfortunately, in 2010, a $325 repo fee had the value of $184 compared to when I entered the business in 1989.

And so, my ranting began.

Frozen for 35 Years

Frozen for 35 Years

From $325 to $350, is not a big leap. Especially after 35 years. Of course, some lenders are paying for dolly and flatbed fees, but storage and personal property fees remain for the most long gone and even with the eminent demise of the CFPB the buffalo, aren’t likely to make a comeback.

As if this stagnancy wasn’t bad enough, that flat ugly $350 just keeps dropping in value as the chart below shows.

So, the cost of a pizza goes up, the cost of a Big Mac and everything else does as well except, of course, the repossession fee.

The Blame Game

So, who is at fault for this fee stagnancy?

Is it the fault of the lenders?

Well, you can’t really blame the lenders for wanting their fees low. It’s what they do. It’s what all responsible businesses do. It’s not like they all get together in some dark room conspiring to keep fees low.

Is it the fault of the forwarders?

Directly, no. The forwarders are competing against each other and price point is one of those elements of competition. Yes, they do dictate what agency gets paid out of that forwarding fee, but they have massive expenses to cover for providing the marketing that the agencies can’t do themselves as well as the insulation from client management that agencies would otherwise have to perform themselves as well.

Forwarders provide valuable services to agencies and lenders that neither can now do well themselves. Lenders live in a world of constant expense management, it’s the nature of banking.

Let’s face it. This problem is mostly self-inflicted. The days of agencies directly marketing themselves to lenders is mostly gone. Most agencies now depend upon forwarder assignments and are ill equipped to self-market well enough to acquire volume at a scale high enough to sustain themselves.

The reality is, lenders will not pay any more for the services of an agency or forwarder than they must. There will be no change in the fees they pay until they can no longer receive services for that price.

Another reality is that as long as there is any profit margin to be had, forwarders and agencies will continue to accept whatever fees they can get.

Musical Chairs

As mentioned, repossession volume is at near record levels for a second straight year and everyone is busy. Lenders, forwarders and agencies are all getting along perhaps better than ever before. And that’s great.

But like in the childrens game of musical chairs, when the music stops everyone must grab a chair or lose. And as with everything, all good things eventually come to an end. One day the assignment and recovery volume will slow. The thin profit margins that were sustainable under a high-volume environment will fail in the face of inflation.

As these failures occur, the number of repo agencies will begin to thin as will the staffing levels at the forwarding companies. We saw this during the pandemic and It will eventually happen again.

And sometime after, years down the line, whoever is left standing when the volume surges again, will have the opportunity to move that fee needle back to sustainable business levels. But of course, some smart Alecs will open up new shops and push it right back down again.

Rinse, wash, repeat.

I can’t say what the solution is, but I’ve accomplished my long overdue venting and I’m done for awhile. Thank you for listening!

Kevin Armstrong

Publisher

Much of this is from my Book “Repo Blood” A Century of Auto Repossession History. This makes a great gift for clients, so order soon to assure delivery before Christmas!

The Big Mac Index and The Repo Fee – The Big Mac Index and The Repo Fee – The Big Mac Index and The Repo Fee – The Big Mac Index and The Repo Fee – The Big Mac Index and The Repo Fee – The Big Mac Index and The Repo Fee

The Big Mac Index and The Repo Fee – Repossess – Repossession – Repossession Agency – Repossessor – Repossession – Repossession History – Forwarder – Lending

More Stories

Auto Credit Is Flowing Again. So Is Future Repo Risk

Think Before You Post – Your Business Depends on It

When the Lender Runs Out of Road: Why Car-Mart’s Problems Could Become Yours

The Growing Insurance Crisis Threatening the Repossession Industry

Why Did I Get Out of the Repossession Business?

Contingency – Looking Back at A War Long Lost